Maine residents are eligible to receive a $25,000 exemption on the total tax assessed value of their primary home, typically saving them several hundreds on their annual municipal tax bill.

Click the following link for a fillable Maine Homestead Exemption Application:

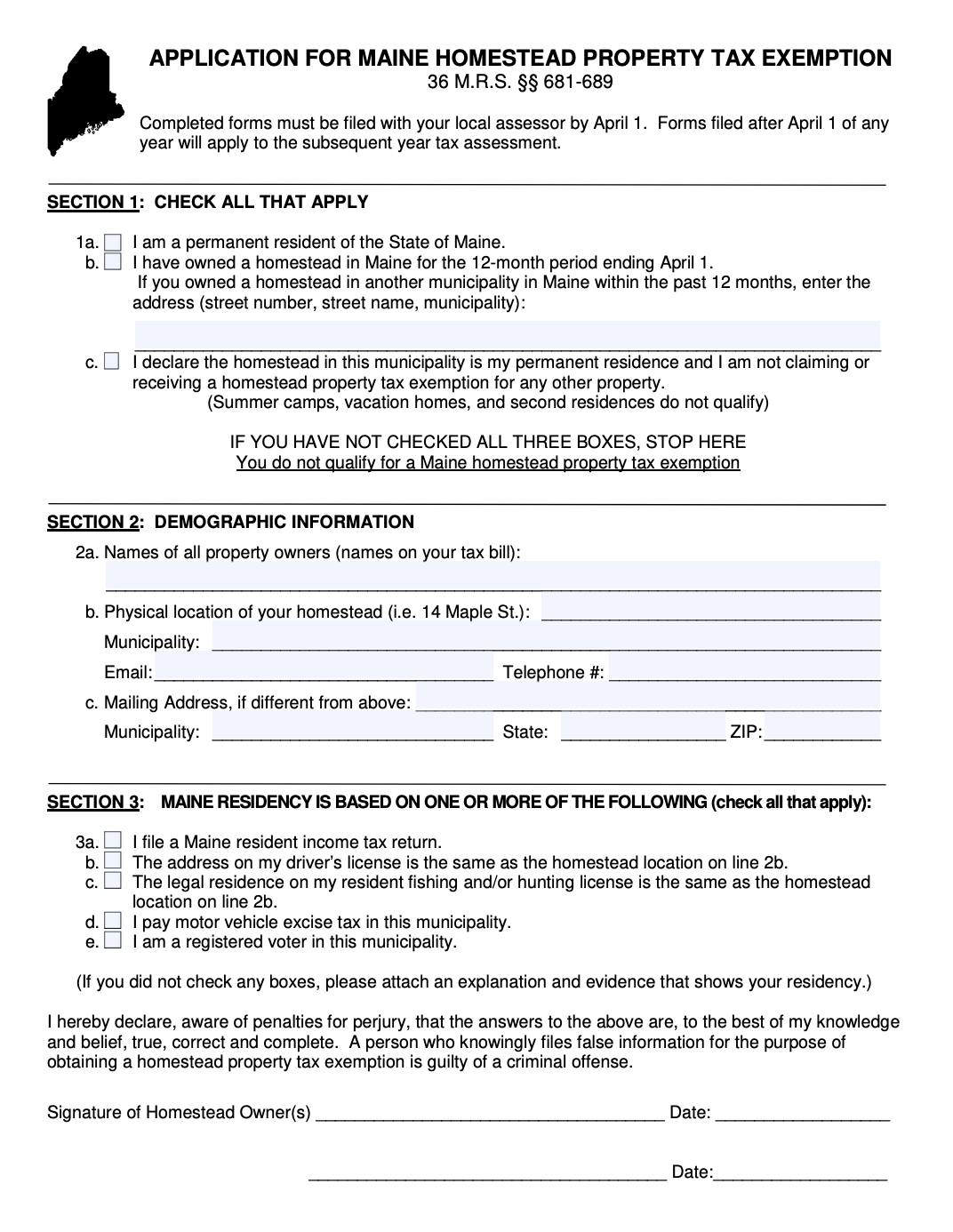

INSTRUCTIONS

SECTION 1. Check the appropriate box related to each question. You must check all three boxes to qualify for the Maine homestead property tax exemption. If you have moved during the year and owned a homestead in Maine prior to your move, enter the address of the homestead you moved from on line 1b. Your ownership of a homestead must have been continuous for the 12-month period ending on April 1. If you did not check all boxes in this section, you do not qualify for the homestead property tax exemption. A person on active duty serving in the Armed Forces of the United States who is permanently stationed at a military or naval post, station or base in this state is deemed to be a permanent Maine resident. A person on active duty serving in the Armed Forces of the United States does not include a member of the National Guard or the Reserves.

SECTION 2. Enter your full name(s) as shown on your property tax bill, the physical location of your home, your telephone number, email address, and your mailing address, if different than the physical location.

SECTION 3. This section gives the local assessor information which may be used to determine if you qualify and should support your answers to the questions in SECTION 1. Please check the appropriate box for each of the applicable statements in this section.

At least one of the owners of the homestead must sign this document. Please file the application with your local municipal assessor. If, for any reason, you are denied exemption by the assessor, you may appeal the assessor’s decision under the abatement statute, 36 M.R.S. § 841.

DEFINITIONS

Homestead. “Homestead” means residential real property owned by an individual or individuals and occupied by those individuals as their permanent residence. Residential real property held in a revocable living trust for a beneficiary who occupies the property as his or her permanent residence also qualifies as a homestead. A resident homeowner who is subject to foreclosure and subsequently purchases the home back from the municipality is considered to have no interruption in homeownership for purposes of this exemption.

Municipality. “Municipality” means any city, town, plantation, or that portion of a county in the unorganized territory.

Permanent residence. “Permanent residence” means that place where an individual has a true, fixed, and permanent home and principal establishment to which the individual, whenever absent, has the intention of returning. An individual may have only one permanent residence at a time and, once a permanent residence is established, that residence is presumed to continue until circumstances indicate otherwise.

Permanent resident. "Permanent resident" means an individual who has established a permanent residence.

A cooperative housing corporation may apply for a homestead exemption to be applied against the valuation of property of the corporation that is occupied by qualifying shareholders. To qualify, the corporation must complete an Application for Maine Homestead Property Tax Exemption for Cooperative Housing Corporations.